Introduction to Blockchain Technology and Its Applications

- Understanding the Basics of Blockchain Technology

- Exploring the History and Evolution of Blockchain

- The Key Components of Blockchain Technology

- Real-World Applications of Blockchain Technology

- Challenges and Limitations of Blockchain Technology

- Future Trends and Innovations in Blockchain Technology

Understanding the Basics of Blockchain Technology

Blockchain technology is a decentralized, distributed ledger system that records transactions across multiple computers in a secure and transparent manner. This technology enables the creation of a tamper-proof record of transactions, providing a high level of security and trust.

One of the key features of blockchain technology is its ability to create a chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, creating a secure and immutable record of all transactions.

Blockchain technology is often associated with cryptocurrencies, such as Bitcoin and Ethereum, but its applications go beyond digital currencies. It can be used in various industries, including finance, supply chain management, healthcare, and more.

By understanding the basics of blockchain technology, individuals and businesses can leverage its benefits to streamline processes, increase security, and improve transparency in their operations. It is essential to stay informed about the latest developments in blockchain technology to harness its full potential in various applications.

Exploring the History and Evolution of Blockchain

Blockchain technology has a rich history that dates back to the early 1990s. It was originally conceptualized by Stuart Haber and W. Scott Stornetta as a way to timestamp digital documents to prevent tampering. However, it wasn’t until 2008 when an individual or group of individuals using the pseudonym Satoshi Nakamoto introduced blockchain as the underlying technology behind the digital currency Bitcoin. This marked the beginning of blockchain’s evolution from a niche concept to a revolutionary technology with far-reaching implications across various industries.

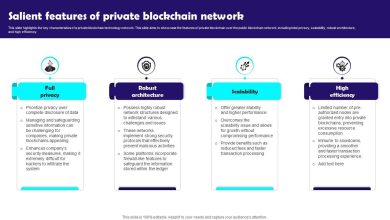

Over the years, blockchain has undergone significant advancements and refinements, leading to the development of different types of blockchains such as public, private, and consortium blockchains. Public blockchains, like Bitcoin and Ethereum, are decentralized networks where anyone can participate, while private blockchains restrict access to authorized users. Consortium blockchains are a hybrid model where a group of organizations controls the network.

The evolution of blockchain technology has also seen the rise of smart contracts, which are self-executing contracts with the terms of the agreement directly written into code. Smart contracts automate and enforce the execution of agreements, reducing the need for intermediaries and streamlining processes. This innovation has opened up new possibilities for various applications beyond cryptocurrencies, including supply chain management, healthcare, and voting systems.

As blockchain continues to evolve, researchers and developers are exploring ways to address its scalability, security, and interoperability challenges. Scalability issues, such as slow transaction speeds and high energy consumption, are being tackled through solutions like sharding and layer-two protocols. Security concerns, such as 51% attacks and vulnerabilities in smart contracts, are being addressed through rigorous testing and auditing practices. Interoperability challenges, which hinder the seamless exchange of data and assets between different blockchains, are being tackled through projects like Polkadot and Cosmos.

In conclusion, the history and evolution of blockchain technology have been marked by innovation, experimentation, and continuous improvement. As blockchain matures and becomes more mainstream, its potential to disrupt traditional industries and empower individuals with greater control over their data and assets will only continue to grow.

The Key Components of Blockchain Technology

Blockchain technology consists of several key components that work together to create a secure and decentralized system for recording transactions. These components include:

– **Blocks**: Blocks are the individual units of data that are stored on the blockchain. Each block contains a list of transactions, a timestamp, and a reference to the previous block in the chain.

– **Chain**: The chain refers to the sequence of blocks that are linked together using cryptographic hashes. This chain ensures that the data stored on the blockchain is tamper-proof and secure.

– **Decentralized Network**: Blockchain technology operates on a decentralized network of nodes that work together to validate and record transactions. This network eliminates the need for a central authority, making the system more resilient to attacks.

– **Consensus Mechanism**: The consensus mechanism is the protocol used to achieve agreement among nodes on the validity of transactions. This mechanism ensures that all nodes in the network have a consistent view of the blockchain.

– **Cryptographic Hash Functions**: Cryptographic hash functions are used to secure the data stored on the blockchain. These functions generate unique fingerprints for each block, making it nearly impossible to alter the data without detection.

By combining these key components, blockchain technology provides a transparent, secure, and efficient way to record transactions without the need for intermediaries. This technology has the potential to revolutionize industries ranging from finance to supply chain management.

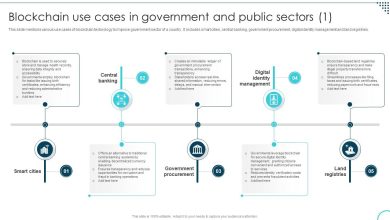

Real-World Applications of Blockchain Technology

Blockchain technology has a wide range of real-world applications beyond cryptocurrencies. One of the key areas where blockchain is being utilized is supply chain management. Companies are using blockchain to track the movement of goods from the manufacturer to the end consumer. This helps in ensuring transparency and authenticity in the supply chain process.

Another significant application of blockchain technology is in the healthcare industry. By storing patient records on a blockchain, healthcare providers can securely access and share patient information, leading to improved patient care and data security. Additionally, blockchain can be used to track the authenticity of pharmaceuticals, reducing the prevalence of counterfeit drugs in the market.

Blockchain technology is also revolutionizing the voting system by providing a secure and transparent platform for conducting elections. By recording votes on a blockchain, the integrity of the voting process can be maintained, ensuring that each vote is counted accurately and cannot be tampered with.

Moreover, blockchain technology is being used in the real estate industry to streamline property transactions. By recording property ownership on a blockchain, the need for intermediaries such as lawyers and brokers is reduced, leading to faster and more cost-effective transactions.

Overall, blockchain technology has the potential to transform various industries by providing secure, transparent, and efficient solutions to complex problems. As more companies and organizations adopt blockchain technology, we can expect to see even more innovative applications in the future.

Challenges and Limitations of Blockchain Technology

One of the main challenges of blockchain technology is scalability. As the number of transactions increases, the network can become congested, leading to slower processing times and higher fees. This limitation has been a major hurdle for widespread adoption of blockchain in industries that require high transaction volumes.

Another limitation is the issue of privacy and confidentiality. While blockchain offers transparency and immutability, it also means that all transactions are visible to anyone on the network. This lack of privacy can be a concern for businesses that deal with sensitive information and need to protect their data.

Security is also a significant challenge for blockchain technology. While the technology is known for its robust security features, there have been instances of hacking and security breaches in the past. These incidents have raised doubts about the overall security of blockchain networks and have made businesses hesitant to fully embrace the technology.

Interoperability is another challenge facing blockchain technology. Different blockchains often use different protocols and standards, making it difficult for them to communicate and share data with each other. This lack of interoperability can hinder the seamless integration of blockchain into existing systems and processes.

Despite these challenges and limitations, blockchain technology continues to evolve and improve. Developers are working on solutions to address scalability, privacy, security, and interoperability issues. As the technology matures, it is expected to overcome these challenges and unlock new possibilities for various industries.

Future Trends and Innovations in Blockchain Technology

The future of blockchain technology holds exciting possibilities for innovation and advancement in various industries. As the technology continues to evolve, we can expect to see several trends shaping its development:

- Increased scalability: One of the main challenges facing blockchain technology is scalability. Developers are working on solutions to increase the speed and efficiency of blockchain networks, allowing for more transactions to be processed in a shorter amount of time.

- Enhanced security: Security is a top priority in the blockchain space. Innovations such as advanced encryption techniques and multi-factor authentication are being implemented to ensure the integrity of data stored on the blockchain.

- Interoperability: As blockchain networks continue to proliferate, there is a growing need for interoperability between different platforms. Projects are underway to create standards that will allow for seamless communication and data transfer between disparate blockchains.

- Integration with other technologies: Blockchain technology is being integrated with other emerging technologies such as artificial intelligence and the Internet of Things. This convergence has the potential to revolutionize industries by enabling new use cases and applications.

- Regulatory developments: Governments around the world are beginning to establish regulatory frameworks for blockchain technology. These regulations will help to legitimize the technology and provide guidelines for its use in various sectors.

Overall, the future of blockchain technology is bright, with endless possibilities for innovation and disruption across industries. By staying abreast of these trends and developments, businesses can position themselves to take advantage of the opportunities that blockchain technology has to offer.